The economic dimension

By Roberto Zoboli, Full Professor of Economic Policy

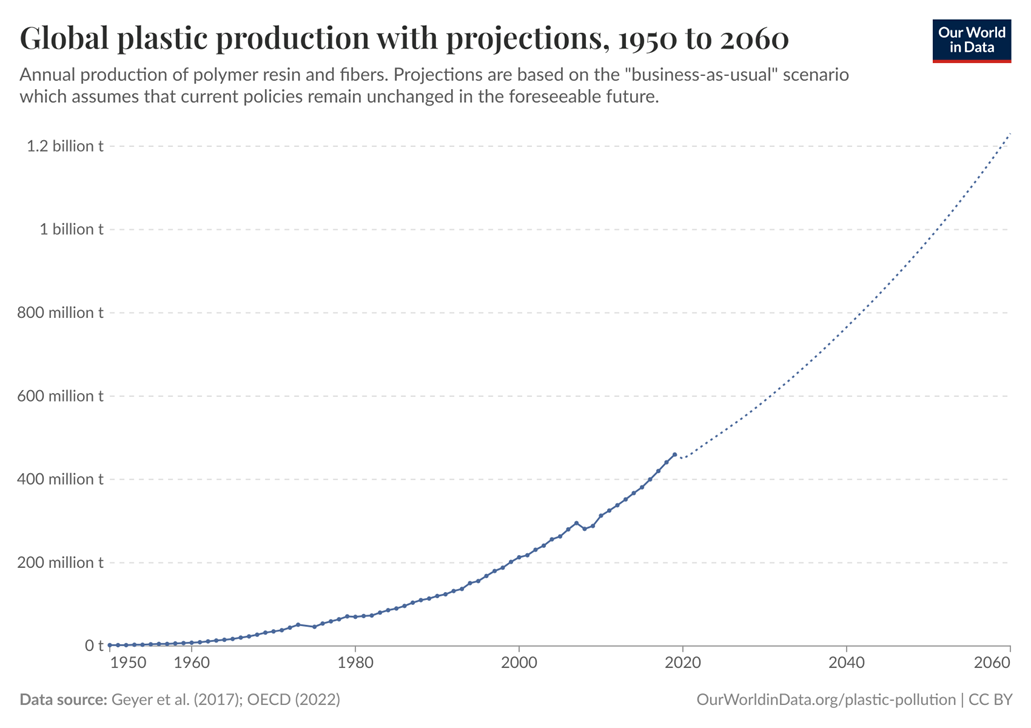

A never-ending trend: plastics production

Since the 1950s, the world's production of plastics has grown tremendously. If trends continue, world production will rise from almost 500 million tons today to over 1.2 billion tons in 2060. The production of primary (virgin) plastics generates about 400 billion US dollars in turnover and 1.2 million jobs worldwide (Oxford Economics). The functional and economic advantages of plastics (durability, low cost, flexibility of use, lightness) are the basis of their great growth but also of the great environmental problems in the management of large quantities of materials that have become waste after use. In 2022, almost 380 million tons of plastic waste were generated worldwide, of which only 38 million tons were recycled (10%).

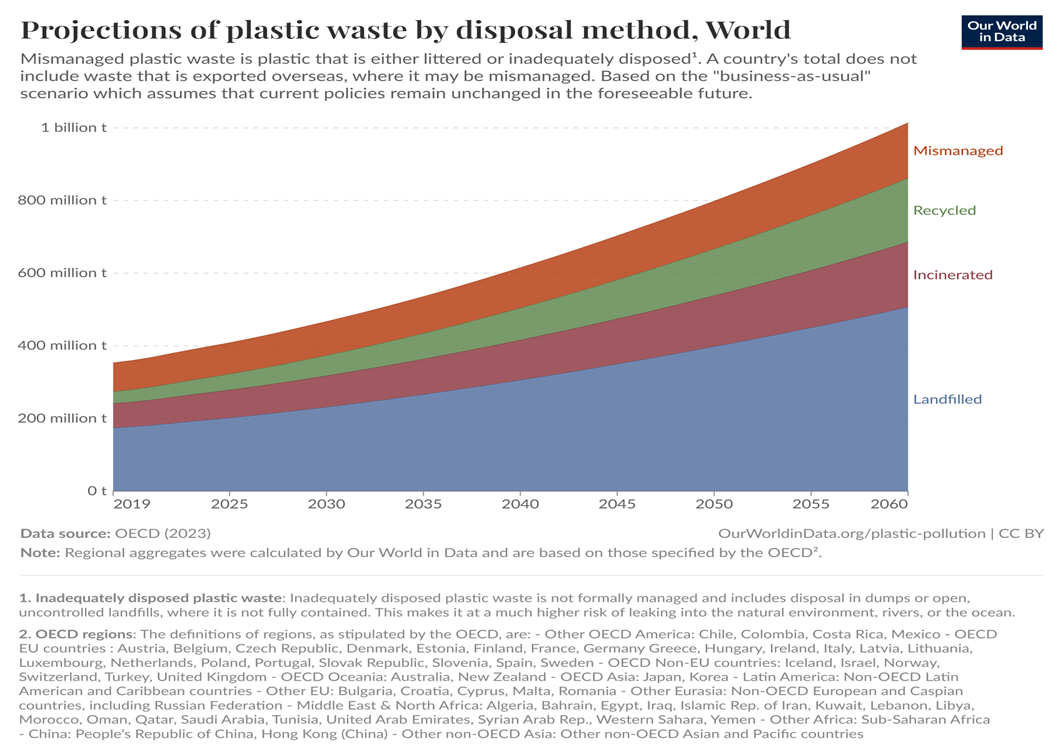

Circles that don't close: recycling and missing reuse

Landfilling is still the prevailing form of plastic waste management on a global scale, and projections indicate that it will continue to be so in the future in the absence of strong actions. An increasing amount is being allocated to material recycling, so much so that the production of recycled plastics grew by 19% in 2018-2022, compared to +9% of total plastics production (Oxford Economics). A large quantity is then destined for incinerators, generally with energy recovery, an environmentally inferior solution to recycling but technically and economically advantageous. The key problem of plastic waste remains 'mismanagement', i.e. 'non-management' or improper management (open air combustion, discharge into the sea and rivers, uncontrolled landfill), which accounts for a share of 22% on a global scale, larger than incineration (19%) and recycling (9%). This amounts to 23 million tonnes spent on the environment (OECD estimates, 2022). As a result, the waste that is most frequently found dispersed in aquatic ecosystems, including those in deep water, is plastic bottles and bags.

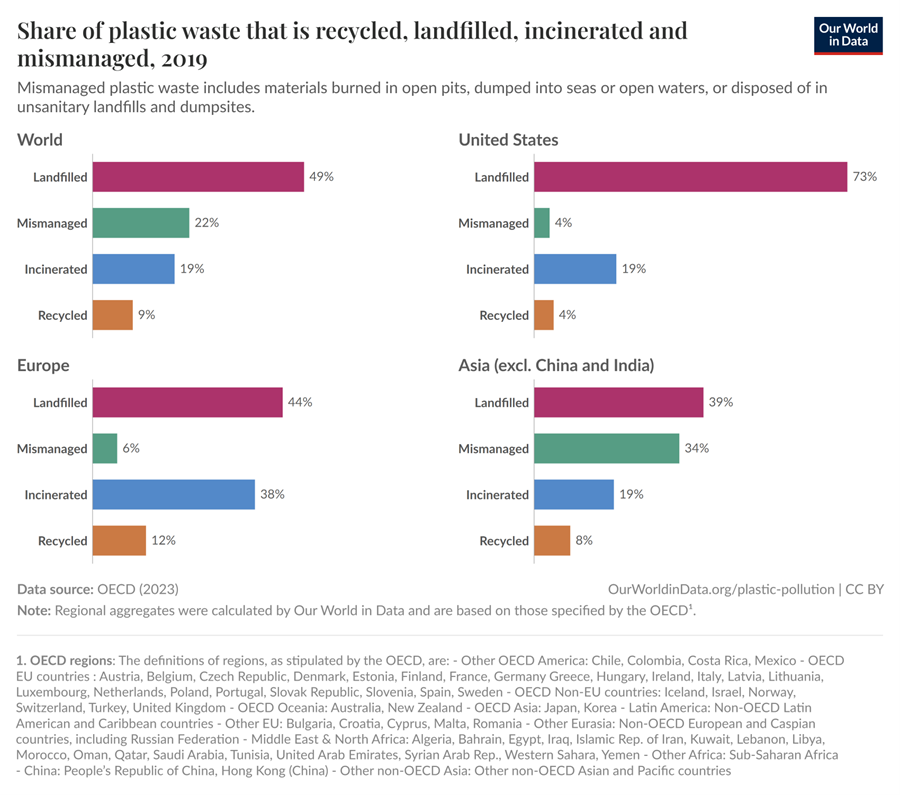

The area with the highest share of mismanagement is Asia (34%) while the share is low in both the United States (4%) and Europe (6%). But the low mismanagement in the United States and Europe is also due to the large export streams of plastic waste that these countries have activated until recent years, particularly to Asia. In this way, mismanagement in certain areas, such as Asia, also depends on the large load of waste they have received from other areas of the world for many years.

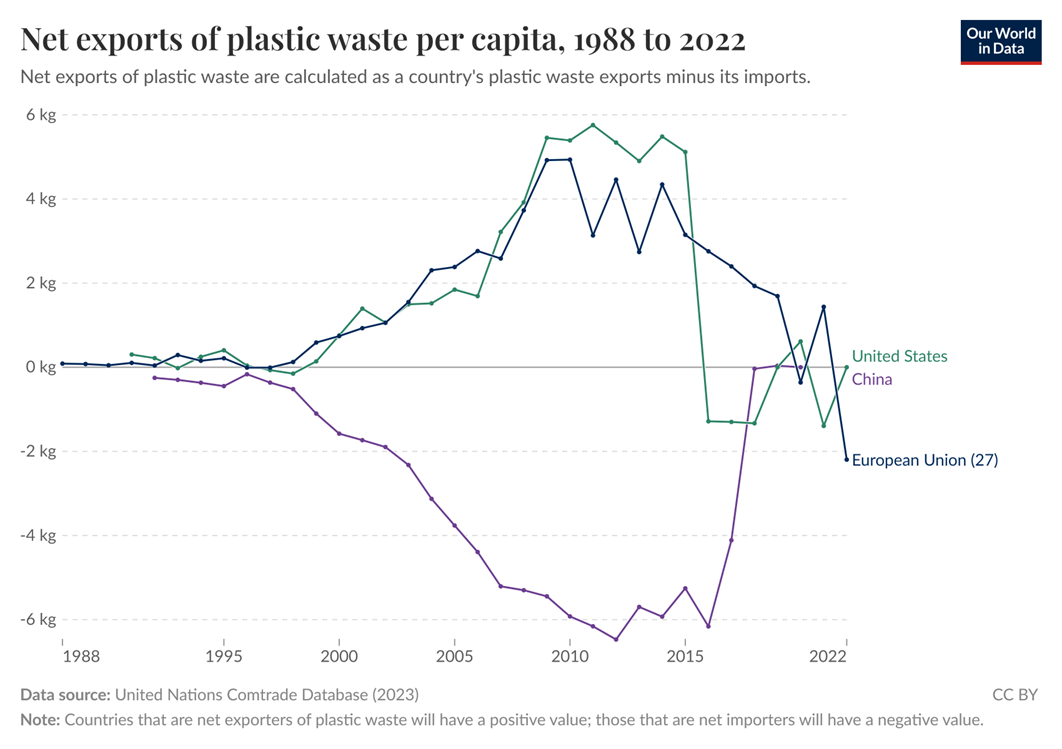

Lost on the streets of the world: plastic waste trade

Since the 1990s, the large production of plastic waste with limited internal management capacities or high recycling and recovery costs has led to a strong growth in international plastic waste streams. At the peak of that growth, both the US and EU27 had net exports of nearly 6kg of plastic waste per capita. Much of it was destined for China, which imported, at its peak, more than 6 kg per capita. In 2018, China closed its borders to plastic waste from other countries, and large exporters had to divert their flows to other low-income countries, or reduce exports by finding other ways to manage them. In recent years, both the USA and the EU27 have become net importers of plastic waste, also to feed, especially in Europe, waste-to-energy plants that lack other material inputs due to the general development of recycling. Millions of tons of unmanaged plastic are still lying around the world.

Economy of the useless: excess plastic packaging

Packaging is the largest use of plastics overall, accounting for more than 30% by volume globally and 40% in Europe. Excess materials in packaging, including plastics, is a phenomenon of everyday experience that has little functional and economic justification, creates costs for consumers, and prepares an excess of post-consumer plastic waste. In Europe, as part of the Circular Economy Action Plan (2020), the new regulation 2025/40 came into force in February 2025, which also aims to combat overpackaging. It includes packaging reduction targets of 5% by 2030 and up to 15% by 2040 and specific measures to reduce plastic packaging waste. From 2030, certain types of packaging will be banned (e.g. for fresh fruit and vegetables, food and beverages in restaurants, single portions and ultra-light single-use plastic bags). There will be limitations on the maximum proportion of empty space in packaging (50% for multi-packs and e-commerce). By 2030, beverage and takeaway food dispensers will have to offer consumers the possibility to use reusable containers and ensure that at least 10% of their products are sold in reusable packaging. All packaging will have to be recyclable, with minimum recycled content targets for plastic packaging. There will also be a requirement to collect separately 90% of single-use metal and plastic containers for beverages up to three litres by 2029.

Is plastic worth it?

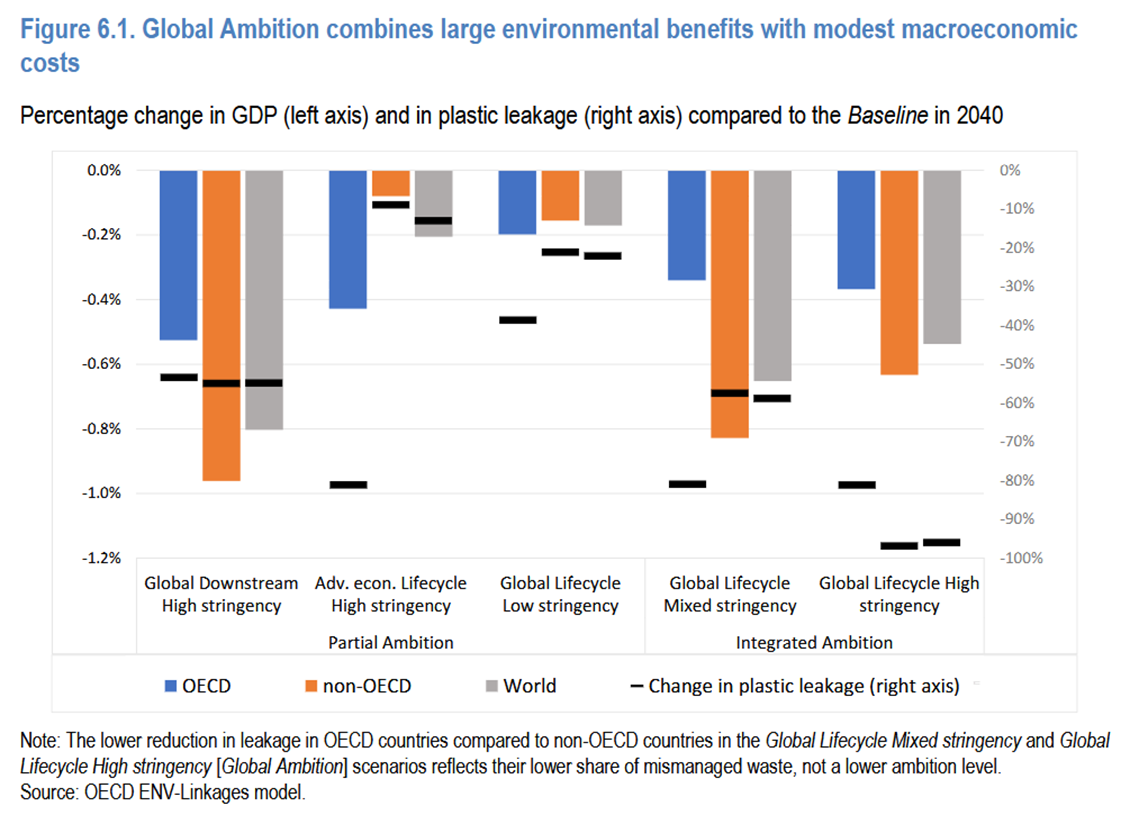

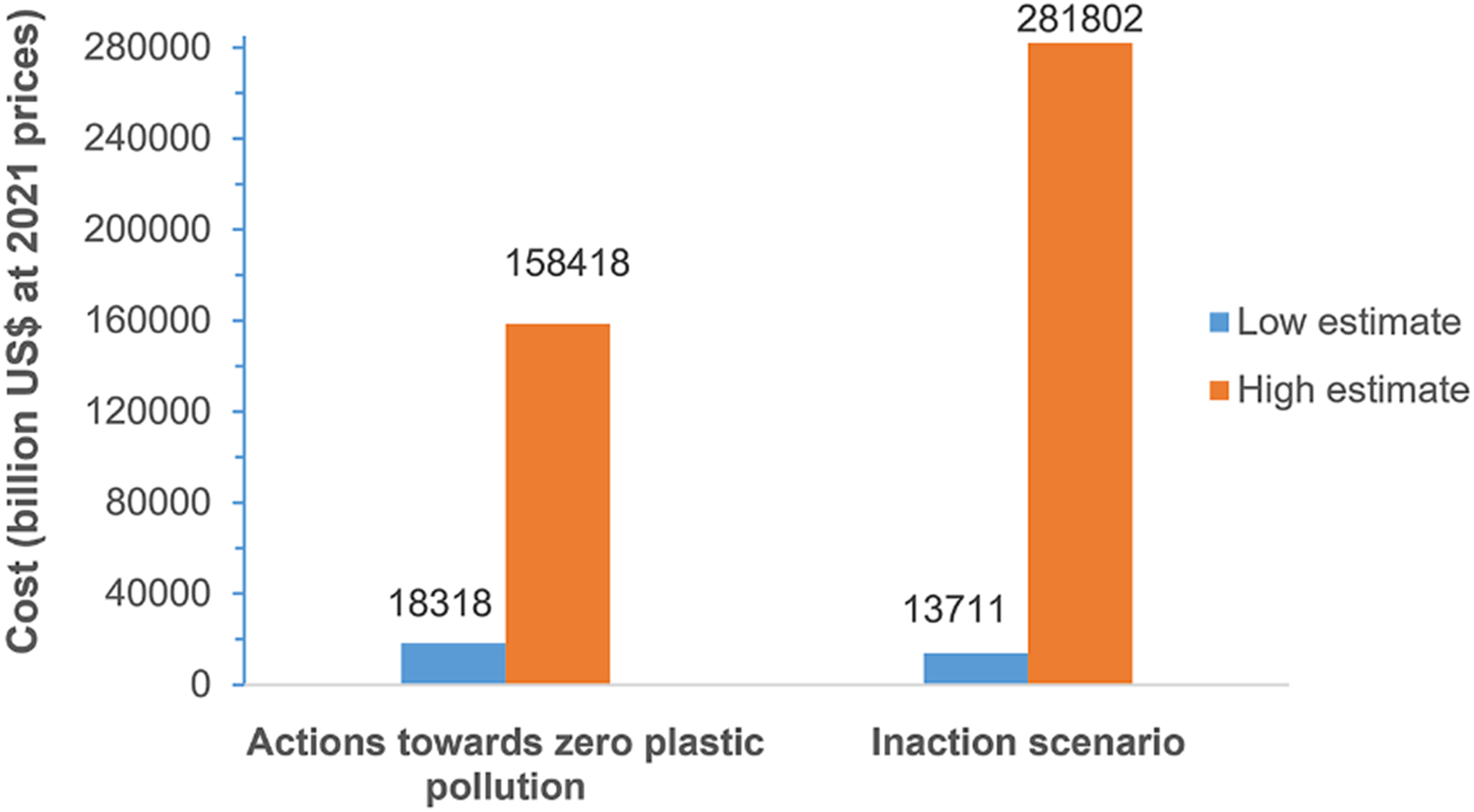

Plastic is worthwhile when it is possible to take advantage of its functional advantages (e.g. lightness, which is good for energy and CO2) and economic advantages (low production costs per unit of function) while minimizing its environmental impacts in production, use and the post-consumer phase, especially when this results in forms of mismanagement. The great economic importance of the plastics sector continues to be a barrier to implementing drastic policies to reduce environmental impacts, especially if they involve the imposition of a limit on production (Oxford Economics 2024). Policies therefore operate on several fronts. In Europe, for example, the directive on single-use plastics (2019), which are subject to great dispersion in the environment, had already banned some plastic products and had introduced, together with the Circular Economy Action Plan (2020), a more extensive application of the principle of 'Extended Producer Responsibility'. In this way, the producer is called upon to take charge of the management of post-consumer waste towards recycling and the use of recycled plastics in new products (e.g. shopping bags). Recent studies quantify the possible economic impact of near-zero mismanagement, including measures to reduce plastic production. Such policies would have an estimated direct economic cost of about 0.6% of world GDP, but would save large ecological costs that can also be monetized (OECD 2024). According to recent estimates, subject to uncertainties in the data (Cordier et al. 2024), the cost of inaction, i.e. the current trend projected into the future without intervention, would be between about $14 trillion and about $282 trillion (trillion dollars) between 2016 and 2040, while the cost of zero plastic pollution policies (including a sharp reduction in production) would be between about $18 trillion and $159 trillion in the same period. If in the minimum estimate there would be an economic loss ($4 trillion), in the maximum estimate there would be a large global economic gain ($123 trillion).

Note: The lower estimates suggest the cost of inaction (US$ 13,711 billion) is slightly cheaper than the one of action (US$ 18,318 billion). However, given the costs and benefits calculated and the missing data (discussed in Section "Discussion and conclusion"), it is not clear that the total cost of action is substantially higher than the one of inaction. Given the incomplete nature of this analysis, it is possible that the total cost of inaction is substantially higher as suggested by the high estimate (inaction cost: US$ 281,802 billion, which is significantly more expensive than action cost: US$ 158,418 billion).

Insights

- Nicola J. Beaumont, Margrethe Aanesen, Melanie C. Austen, Tobias Börger, James R. Clark, Matthew Cole, Tara Hooper, Penelope K. Lindeque, Christine Pascoe, Kayleigh J. Wyles, Global ecological, social and economic impacts of marine plastic, Marine Pollution Bulletin, Volume 142, 2019, 189-195, ISSN 0025-326X

https://doi.org/10.1016/j.marpolbul.2019.03.022. - Cordier M, Uehara T, Jorgensen B, Baztan J. Reducing plastic production: Economic loss or environmental gain? Cambridge Prisms: Plastics. 2024; 2:e2. doi:10.1017/plc.2024.3

https://www.cambridge.org/core/journals/cambridge-prisms-plastics/article/reducing-plastic-production-economic-loss-or-environmental-gain/99BEE1E1A6C185B79CD2735B02C59AC6 - European Parliament, How to reduce packaging waste in the EU

https://www.europarl.europa.eu/topics/en/article/20231109STO09917/how-to-reduce-packaging-waste-in-the-eu-infographics - European Parliament, Plastic in the ocean: the facts, effects and new EU rules

https://www.europarl.europa.eu/topics/en/article/20181005STO15110/plastic-in-the-ocean-the- facts-effects-and-new-eu-rules - Minderoo Foundation, The Price of Plastic Pollution: Social Costs and Corporate Liabilities

https://www.beyondplastics.org/reports/the-price-of-plastic-pollution - OECD, 2024, Policy Scenarios for Eliminating Plastic Pollution by 2040

https://www.oecd.org/en/publications/policy-scenarios-for-eliminating-plastic-pollution-by-2040_76400890-en.html - Oxford Economics, 2024, Mapping the Plastics Value Chain: A framework to understand the socio-economic impacts of a production cap on virgin plastics, Commissioned by The International Council of Chemical Associations (ICCA)

https://www.oxfordeconomics.com/resource/mapping-the-plastics-value-chain/ - UNEP, Our planet is choking on plastic

https://www.unep.org/interactives/beat-plastic-pollution/